Revisiting the fat protocol thesis

In my previous post, we explored how stablecoins are exploding in multiple adoption metrics. In this piece, we will explore whether stablecoin adoption is fuelling a rise in the price of Ethereum as an asset. A commonly held belief in the industry is investing in layer ones will likely create more value than investing in applications. This is because as adoption in the application layer increases, transactions on the main-chain, which in turn increases the demand for the asset powering it. Joel Monegro captured how speculation, boom-bust cycles and early adoption leads to loops that create a rise in the price. I strongly suggest reading his piece from 2016 for more on this. For now - we will look at a critical statement from the piece.

What’s significant about this dynamic is the effect it has on how value is distributed along the stack: the market cap of the protocol always grows faster than the combined value of the applications built on top, since the success of the application layer drives further speculation at the protocol layer - Joel Monegro

With that in mind, let’s take a look at what has been going on with stable-coin market caps.

A likely Flippening

Tether’s massive issuances over the past few months have meant that the gap between the total market capitalisation of major stablecoins (combined) and that of Ethereum’s has been slowly closing. To see how this has panned out - I considered exploring what percentage of Ethereum’s market cap have been held by stable coins. The idea was quite simple. If the fat protocol thesis does stand, Ethereum’s market-capitalisation should be increasing alongside those of the stablecoins on it. Why? Because coin issuance is plugged to consumer demand, which in turn means more transactions and thus more demand for gas. The interesting bit is - this much has already transpired. Tether is routinely one of the highest gas-consuming applications on Ethereum today. However, that has not caused a rapid increase in price even as DeFi establishes itself as a new market segment. I believe there are two reasons for this

1. Unlike “utility” tokens that provide compute or storage-related services, stable coin market-capitalisation represents a dollar figure held in a bank account. A rich enough entity (like an exchange) can choose to collateralise with their idle assets (e.g.: Bitcoin) and release stablecoins without (i) network effects or (ii) token economies a conventional asset has. Both of which are critical components for spurring activity in layer one.

2. Stablecoin issuance can increase rapidly (eg: the past three months) without the base layer reflecting a change in price due to the activity. My belief is that there is likely a lag in the layer one token price catching up the newfound demand.

Looking at market-capitalisation on its own does not give a holistic picture. Therefore, I considered exploring the volume & token-velocity as a measure of transaction frequency.

The Moneyness of ETH

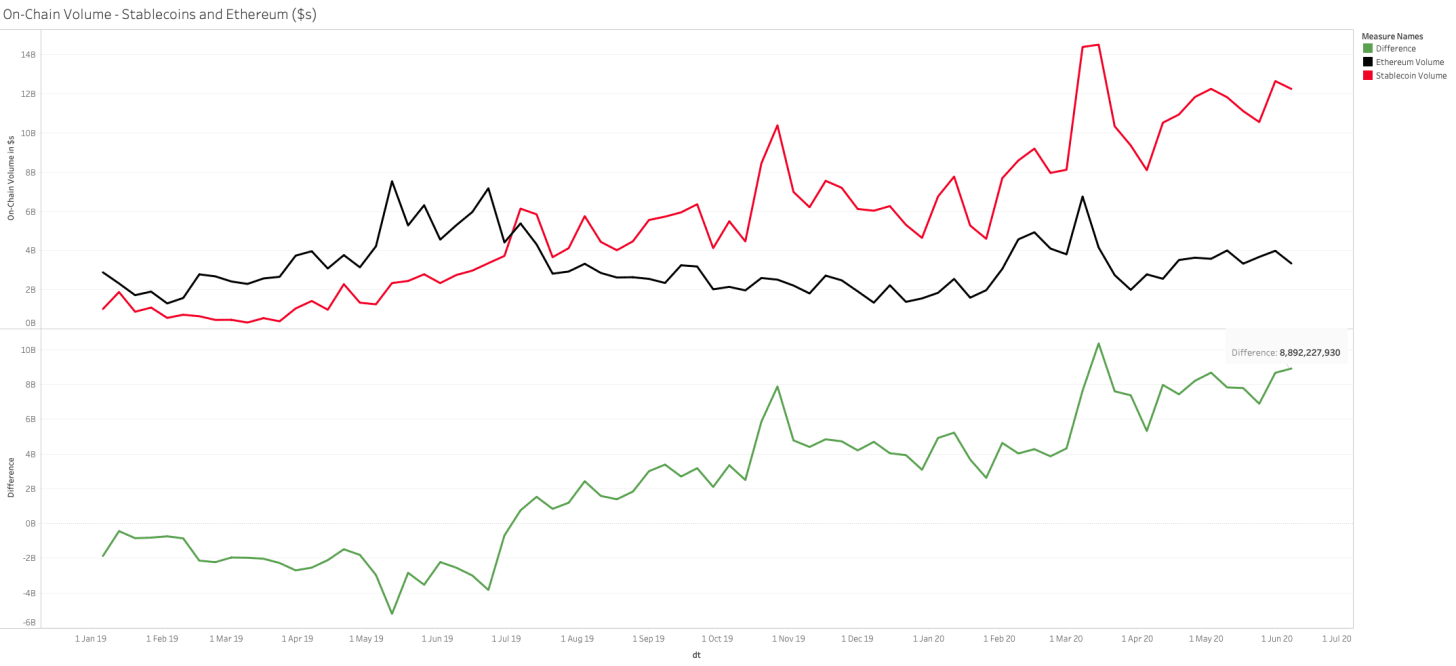

The next bit to consider exploring was how on-chain volume has changed over time. I understand this is a bit of an unfair chart as I am not considering the dollar value of the ERC-20 assets (e.g: Golem, Augur, SONM, Synthetix etc.) that is moved on-chain but simply Ethereum against stablecoins. What I wanted to know was how the gap between the volume of on-chain transfers of Ethereum and stable coins has evolved. Part of the reason to explore this is to consider the moneyness of Ethereum. If public perception of Ethereum is that it is indeed money, then it is fair to assume that there may be a higher volume of Ethereum moving on-chain than that of stable-coins. However, this has not been the case. Individuals seem to be more comfortable holding and remitting large chunks of stablecoins instead of Ethereum. If we notice the chart, this transition happened around July last year as (i) transition of USDT to Ethereum’s standard occurred (ii), and the market rallied. The gap between dollar value moved on Ethereum and those on stable-coins every day has steadily increased. The wider the difference, the lower chance that individuals choose to switch to Ethereum.

Does this mean Ethereum is not money? The argument stands that ETH can be used to receive DAI and therefore is an abstraction of money. More importantly, it is used as the enabler for the transaction and settlement of stablecoins and is consequently still useful. As retail users understand the broader ecosystem in DeFi - they likely switch to the base layer asset. For now, traction is sticky on the application side. We have some reason to believe the trend may remain that way for now.

Playing Catchup

To understand how stablecoins are contributing to Ethereum’s ecosystem, I studied the number of active addresses over the year. To make a fair comparison, we need to observe

- The growth of Ethereum’s active addresses against that of stablecoins over the year

- The percentage of active addresses on Ethereum that comes from stablecoins.

If you notice the chart, you will observe that stablecoins have gone from sub ~10% of total active Ethereum addresses to close to 40% at this point. As the dominance stable-coin addresses have in the network increases, it becomes clear that much of the growth in Ethereum today is fuelled by stablecoins. I assume that if other “utility” networks like those focusing on storage, network and the like is a decade away from existing don’t come to market, DeFi applications will be the source of much of Ethereum's usage. As the dominant layer one chain today, Ethereum will also likely influence where many of the newer players like Polkadot will also focus. Finally, even in terms of actual usage, stablecoins like Multi-collateral DAI is being “used” more than Ethereum today. To check this, I compared the velocities of Ethereum and DAI over the past six months. From Santiment. They define velocity as a measure of the number of times a token is used in a day.

One way to argue against this is that much of ETH’s supply likely lies idle as individuals hodl it in secure wallets and avoid moving it around often. DAI in comparison is used by DeFi power users who move it between vaults, dex’s and other applications on a routine basis. That said - it does show that stablecoins like DAI are actively transacted with quite more than the base layer itself.

Food for Thought

As applications come to market, it is becoming clear that adoption alone is not driving the price of Ethereum any longer. There is likely a lag in price due to

(i) the sector being in the late stages of a bust and

(ii) value transactions occurring on stablecoins without Ethereum being locked up.

Even in DeFi platforms like compound today, lending demand for USDT is often higher than Ethereum. None of this is to suggest the Fat Protocol Thesis is wrong. However, it may need certain accommodations for the fact that application layers that are capital intensive like DeFi may very likely end up requiring it to be updated. My bet is that stable-coin market-cap will likely be higher than that of Ethereum’s over the next year as long as Tether doesn’t blow up. More importantly, if DeFi continues to deliver on traction, a basket of DeFi related projects (eg: Kyber, 0x, Snx) will likely have a higher combined market-cap than that of Ethereum over time. Maybe, we really do obsess over the base layer a bit too much. Maybe, the next generation of token enthusiasts will argue over applications instead of the settlement infrastructure.

Have a pleasant weekend.

Joel John

Conversations (0)