DeFi & Demand: Part I

It seems like everyday new products, protocols and approaches on how to use and view crypto currency are being introduced and or refined. This often leaves me wondering how all this new information will shift the way we view economics as a whole. So, my aim here is to further expand upon some of my pondering over the course of a few articles. I felt it best to take things a step at a time rather than force everything into 2,500 words. With any luck, this may make things easier for me to define, easier for others to follow and allow for some to offer input if so inclined.

But before I begin, a few things require clarifying in regards to my previous article (and preface to this series) titled “A Peek into Ethereum Token Activity.” First, my use of the phrase “activity and demand” was somewhat redundant and therefore misleading. According to my thoughts, activity is the amount of coins/tokens being demanded by market participants. So moving forward, I’ll refer to the same theory as DeFi & Demand, I know, it’s very catchy and almost overwhelmingly clever.

Another thing I have to point out is that this is modeled after a theory, not a law as I incorrectly stated in my prior writing. It’s important that I make this distinction clear, for in the off chance that I am horribly wrong, I can fall back on this later.

Ok, so now let’s get on with it. You may notice that I’ve taken a few liberties pertaining to the figure presented below. Since this theory is an adaptation of economic equilibrium, based off of supply and demand, I felt it best to appropriate that model and modify it to suit my needs.

This mechanism functions in a number of ways: the higher the price, the lower the amount of active coins market participants will demand/offer, and the higher the price, the greater the quantity market makers/miners (and in some cases retail) will aim to add to circulation or deploy from DeFi. With that said, we can start to imagine how these curves might endlessly vary, in slope and so too in appearance. And while for the most part the circulation curve trends up, it’s important to remember that the ongoing growth and development of decentralized finance will help add the required variance to circulation curves.

In an attempt to offer further clarity let’s consider how Steven Levitt, the author of Freakonomics, describes supply & demand;

“If the price of a good goes up, people demand less of it, the companies that make it figure out how to make more of it, and everyone tries to figure out how to produce substitutes for it. Add to that the march of technological innovation.”

For instance, in the case that I am describing just replace ‘goods’ with ‘Ethereum,’ then replace ‘demand’ with ‘token activity,’ and instead of companies think of those with some control over supply, such as market makers, miners/validators and those participating in DeFi. Finally, I think we all know who the substitutes and imitators are.

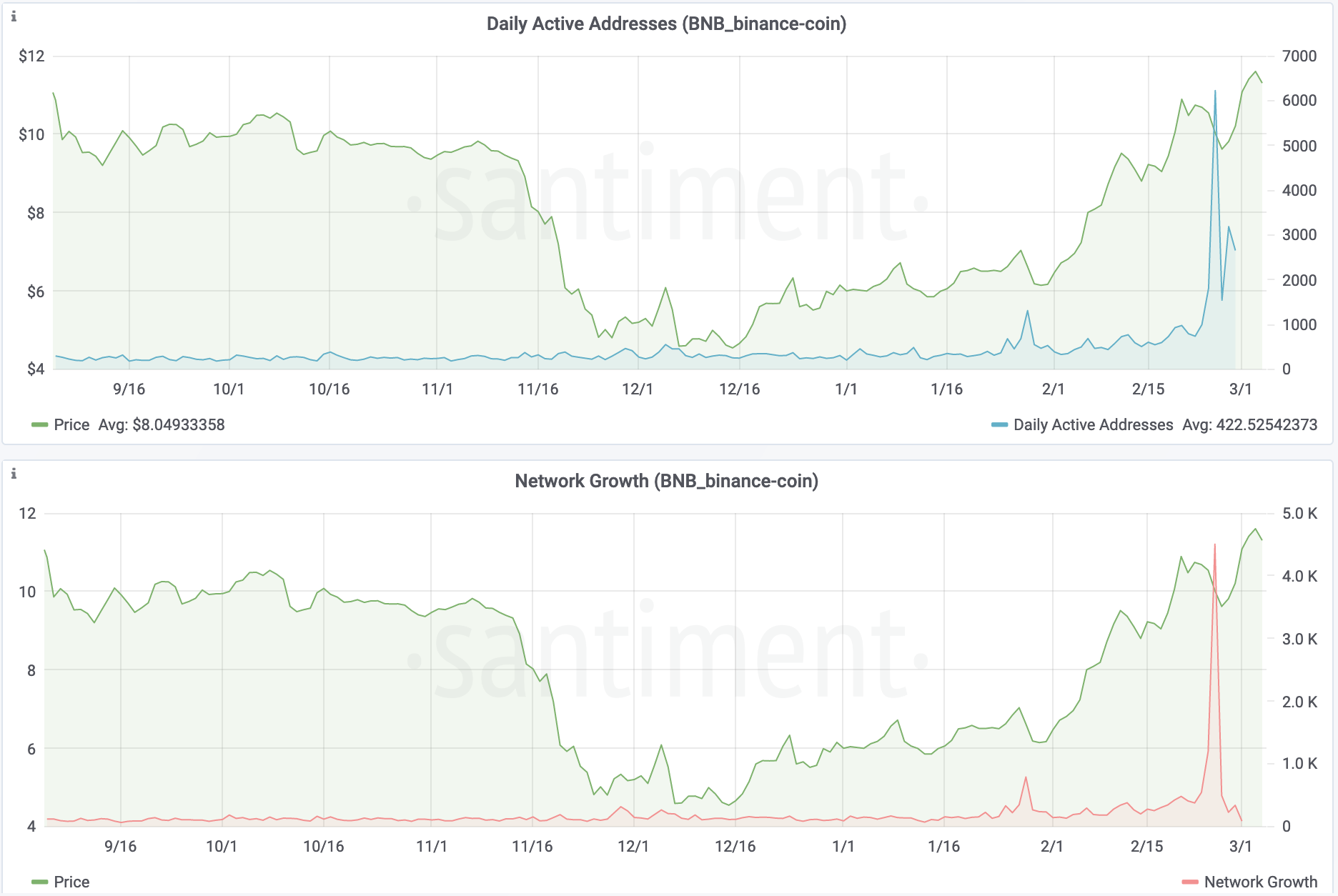

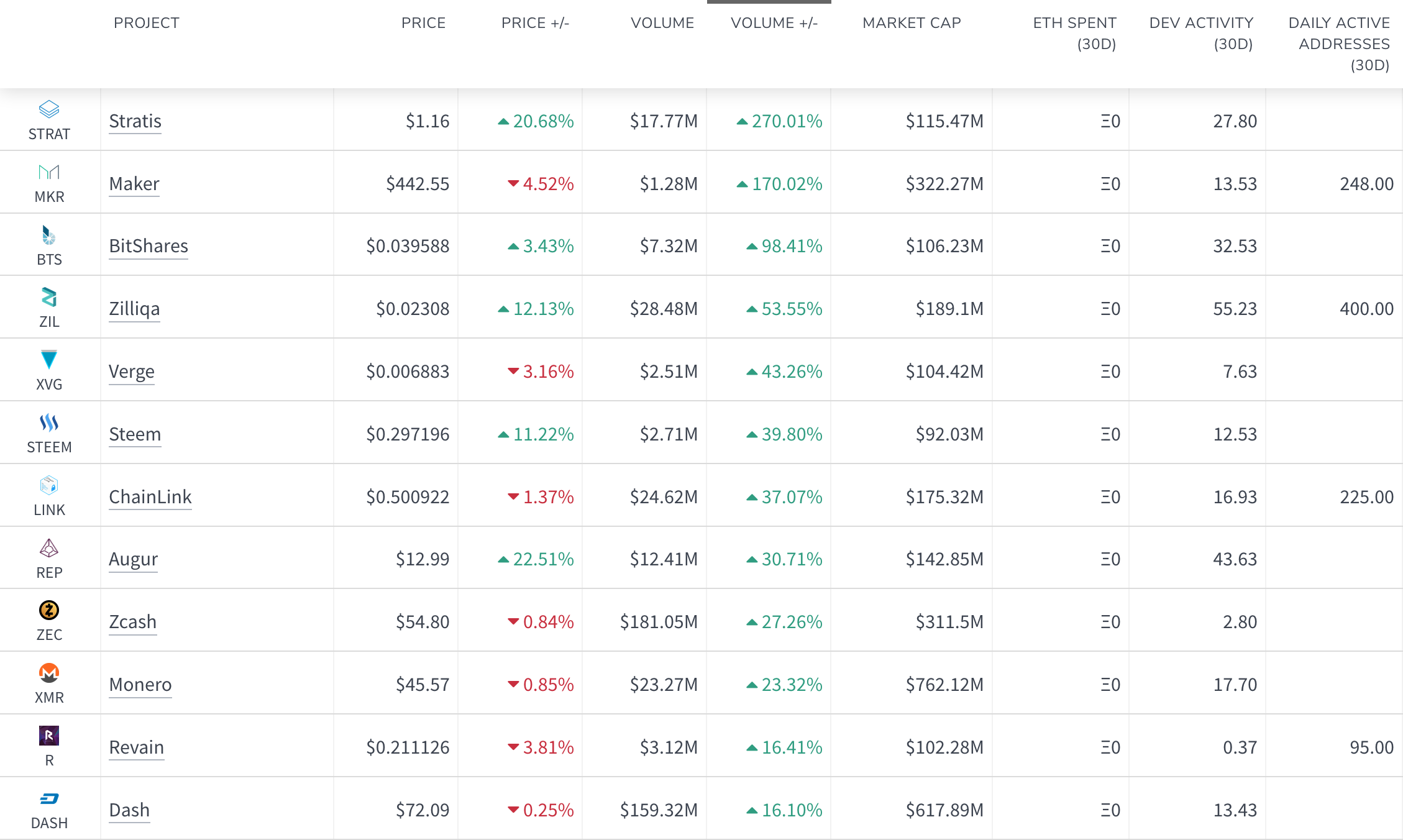

Moving on, here are a few examples to help illustrate some of these points:

It’s crucial to remember that staking and locking ETH in smart contracts will allow for artificial regression to the overall circulation curve. Likely, other things will come along that may have this effect as well. Keep in mind, such curves will be fluctuating and not likely coupled to one another.

Now we can see that even with a constant addition to supply the overall trend of active tokens remains down, with a larger degree of volatility as well. Suffice to say it also appears there has been much discrepancy in terms of valuation. Furthermore, since we can define distinct ranges, like 1 year or 90 days, we are also able to view different degrees of variance in activity and how that relates to price action. (see below)

But, why does any of this matter? Well first and foremost, I believe these ideas may display how Ethereum’s ecosystem is evolving into one that is increasingly dynamic. Meaning, in the future we might see a more robust form of value transfer on the platform as both inflationary and deflationary aspects gain greater foothold. Second, if these curves interact as I am positing we may be able to effectively predict future price movements by observing them.

So there you have it, the introduction to something I have spent far too much time thinking about, researching and discussing with peers. All things considered, I wanted to make sure that these thoughts were well outlined prior to posting and before diving deeper with some in depth examples. In the next part I’ll look to expand upon the relationship between ETH locked in smart contracts, percent of tokens active and price.

Conversations (0)